|

Corporate Social Responsibility and

Impact on Profitability of Banks in

the United Arab Emirates

Saigeeta

Kukunuru (1)

Sonia Singh (2)

(1) Dr. Saigeeta Kukunuru School of

Business, (Asistant Professor) City

University college, Ajman

(2) Dr. Sonia Singh School of Business

(Adjunct Faculty), University of Jazeera,

Dubai

Correspondence:

Dr.

Sonia Singh School of Business (Adjunct

Faculty),

University of Jazeera, Dubai

Email: sonia23singh@gmail.com

Abstract

Profitability is a key performance

indicator that UAE banks measure periodically.

However, the UAE commercial and Islamic

banks differ in the profitability

policy and pursuit as this illustrates

the effectiveness of the organizations'

operations. A common practice by banks

globally and in the UAE, is Corporate

Social Responsibility (CSR) to the

stakeholders and environment. Banks

engage in pyramid, intersecting cycles

and concentric circles CSR models

to win and retain clients, whose loyalty

accounts yield higher profits. Moreover,

CSR creates a positive image among

bank customers who associate to be

part of the social, environmental

and sustainability initiatives and

courses. This implies that CSR makes

banks disclose their financial performance

information better than their counterparts

that are profitable. In terms of methodology,

this study adopted the KLD approach

where banks profitability performance

is measured as sum of direct and indirect

CRS investments and business. In the

UAE, just like the rest of the world,

profitability is defined by the Return

on Equity (ROE), Return on Assets

(ROA), Net Income to Sales, Earnings

to Sales, Operating Profit to Assets

(OPAT) and Return on Capital (ROC).

This research explored previous positions

that CSR has positive and significant

correlation with UAE banks' profitability.

The analysis study of Abu Dhabi Commercial

Bank, Abu Dhabi Islamic Bank (ADIB)

and Emirates Islamic Banks' CRS impacts

on profitability were concluded to

be either low impact or insignificant

Key words: CSR, profitability,

Islamic banking, KLD approach, financial

performance,

Introduction

The term Corporate Social Responsibility

(CSR) is very broad and varies with

stakeholder participation and objectives.

Generally, CSR entails how organizations

manage their workers' welfare and

rewards, embrace diversity, adhere

to tenets of human rights and minimize

harmful operations and effects to

the environment and society (Blowfield

&Murray, 2008; Carroll, 1979).

Additionally, CSR entails how organizations

govern their activities, legal obligations,

economic transparency and ethical

dispensation (Freeman, 1984). In many

analyses, these CSR practices are

embraced systematically and become

the organization's culture (Hawa,

2012). However, in exceptional circumstances,

some firms embrace a cluster of these

CSR activities based on external pressure,

for example issues to do with pollution

of environment (Bolton, 2013).

A Corporate Social Responsibility

Disclosure Index (CSRDI) is a tool

used to determine criteria that organizations

use to achieve various financial performance

metrics including profitability. A

typical CSRDI is composed on the organization

having vision and mission, board of

directors and top management focus,

products and services, charitable

and welfare activities, employee focus,

debt management, community projects

environmental conservation, legal

and statutory supervision (El-Mosaid

& Boutti, 2012).

Whenever banking institutions have

been at the centre of some past global

financial crisis, their profitability

was affected by the operational and

policy decisions (Bolton, 2013). Among

the actions that banks implemented

to reposition their images and brands

was engagement in CSR and those in

the UAE have embraced the band wagon.

There are two aspects of CSR with

relation to banks profitability (Orlitzky,

et al., 2003). First, CSR can attract

more customers to banks and this can

improve their profit values (Arshard,

et al., 2015). The hypothesis that

banks that act responsibly create

a sense of satisfaction of sound management

and secure financial deposits which

many clients would like to associate

with all the time has been proved

(Scholtens, 2009). One of the few

studies that contradict this position

was by Ahmed, et al., (2012).

Second, CSR is itself a capital intensive

process and can affect the profitability

of the bank. There are arguments that

banks should therefore focus on their

core activities and only allocate

a small percentage of resources towards

CSR as a risk management strategy

(Bolton, 2013). Research shows that

some bank managers are likely to spend

more resources on CSR at the expense

of growing the profitability (Cai,

et al., 2012). Such banks have a policy

that more investments in CSR could

lead to a more positive image and

reputation, whereas the initiatives

diminish the profit margins because

of need for extra operational costs

(Barnea and Rubin, 2010). In fact

a study established that a bank's

investment into CSR lead to its collapse

and ultimately liquidation because

of diversion from core business and

concentration on the public relations

exercise (Sigurthorsson, 2012). Another

study established that over compensation

of employees as a form of CSR places

banks to liquidity risks which eventually

affect their profitability (Gande

& Kalpathy, 2012).

Past Studies on Effect Of CSR on Profitability

Whereas most studies on impact of

organizations CSR have been on market

environment, staff compensation, performance

and other tangible and intangible

forms of goodwill (Bolton, 2013),

very few have covered banks and profitability,

especially in the UAE. Various studies

before the turn of the century indicate

a positive relationship between CSR

activities and banks performance often

summarized by their profitability

(Griffin & Mahon, 1997). The same

trend was observed in successive studies

after the year 2000 (Orlitzky, et

al., 2003; Deckop, et al., 2006).

Even more recently, research shows

that banks with elaborate CSR tend

to perform better than their counterparts

(Shen & Chang, 2009).

Research shows that when banks have

liquidity problems, this affects their

profitability and ability to invest

in CSR, yet potential capital investors

prefer to engage with banks that have

strong CSR initiatives to the society

(Anderson & Meyers, 2007). This

view was upheld by El Ghoul, et al.,

(2011) who added that banks with articulate

CSR can access credit at low interest

rates, have better risk management

and generally positive valuation,

all leading to better profitability.

Moreover, banks with formidable CSR

have good capital flows from client

and stakeholder deposits and this

enables management to explore more

investment products and higher profitability

(Cheng, et al., 2011).

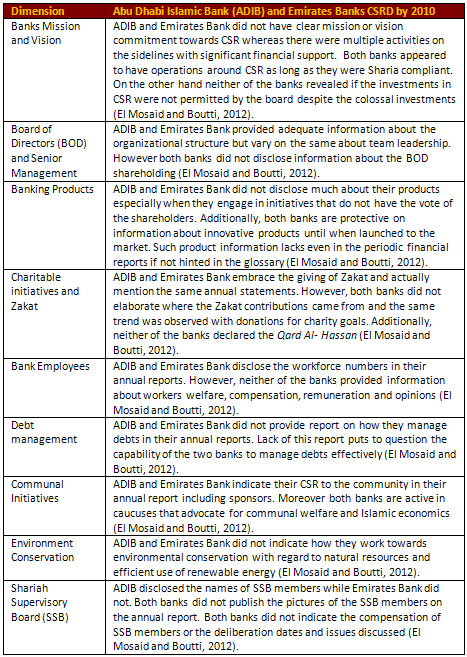

El Mosaid and Boutti (2012) conducted

a study on the effect of CSR to financial

outcomes of Islamic Banks. Among the

UAE institutions included in the study

which are operated under Islamic banking

regulations are Abu Dhabi Islamic

Bank (ADIB) whose CSRD Index was 26.83

and Emirates Islamic Bank CSRD Index

25.61, both in 2010. The following

table is a summary of the CSR dimensions

as applicable in Islamic banks in

the UAE.

Table 1: Islamic Banks CSR Dimensions

Summary

For regression analysis, El Mosaid

and Boutti (2012) chose two profitability

attributes, namely, Return on Assets

(ROA) and Return on Equity (ROE) in

relation to the CSR Index. During

the year 2010, the ROA for ADIB was

1.47% while that of Emirates Bank

was 0.21%, both better than the previous

year. Additionally, the ROA for ADIB

was 12.63% while that of Emirates

Bank was 2.09% in 2010. However, the

ANOVA test for all the tested banks

profitability performance including

ADIB and Emirates Banks established

p-value for ROA at p=0.489>0.0005

in 2009 and p=0.036>0.0005 and

these imply there are no statistically

significant effects of Islamic Banks

CSR on profitability. Additionally,

the NOVA test established p-value

of 0.6555>0.0005 in 2009 and p=0.078

>0.0005 which implies no statistically

significant impact on ROE on CSR.

CSR Activities

of Commercial Bank in UAE

ADCB Corporate Social Responsibility

Activities: In the last two decades,

there are specific challenges that

ADCB was facing that necessitated

board and management to implement

some CSR steps towards better profitability

(ADCB, 2010). These are broadly in

areas of board efficiency, management

capabilities, financial disclosures

and investors and customer relations

(IFC, 2010). The table at appendix

II illustrates some of the ADCB challenges

and the changes undertaken by the

bank. The ADCB started engaging in

CSR from the turn to this century

with the realignment of their products

and services geared for higher profitability.

Therefore, ADCB reorganize the board

followed by the management then specific

operational aspects such as accounting

transparency (ADCB, 2010). Nevertheless,

as the ADCB sought to match the best

practices globally and to remain competitive,

the corporate governance aspects were

also reviewed. The objective of ADCB

was to become a national and regional

role model for other banks. In the

last quarter of 2007, the IFC carried

out an evaluation to establish how

ADCB manages their CSR and governance.

Earlier on, ADCB had implemented various

CSR policies aimed at strengthening

the business operations and performance

within the society (IFC, 2010).

Among the changes brought about by

the CSR were more transparent roles

of the managers, board members and

selection of directors. Moreover,

ADCB started a system of cooperation

between the managers and board members

to ensure banking risks are communicated

and mitigated in time. The ADCB started

a system where the stakeholders would

get regular disclosure reports after

audits in compliance with IFRS (IFC,

2010).

ADCB is involved in various community

investments initiatives towards CSR.

Most of these CSR investments operate

under Memorandum of Understanding

between ADCB and the community as

beneficiary. In 2013, nearly 2,200

homes were renovated while 37, 000

windows were fixed to prevent children

falling through (ADCB, 2013). ADCB

appreciates the need for supporting

communities via fund collection at

their ATMs and online portals. ADCB

is involved in various health and

safety initiatives under CSR umbrella.

ADCB promotes works with Sheikh Khalifa

Medical City staff to create awareness

about different ailments on specific

open days where the banks employees

also benefit from free heart check-up

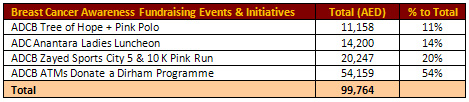

(ADCB, 2013). The following table

illustrates the sources of fund for

the breast cancer campaigns.

Table 2: ADCB mobilization of funds

to fight breast cancer in 2013

Source: (ADCB, 2013, p.48).

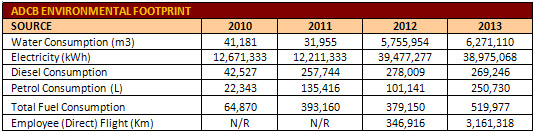

ADCB collaborates with different

stakeholders with agendas on environmental

conservation. Among the bodies working

with ADCB is Environ's services to

manage electronic waste like all old

electronic devices like computers,

wires, mouse, printer and many more

and ensure the bank adopts green initiatives.

The following table illustrates the

ADCB environmental footprints.

Table 3: ADCB Environmental Foot

Print

Source: (ADCB, 2013, p. 50).

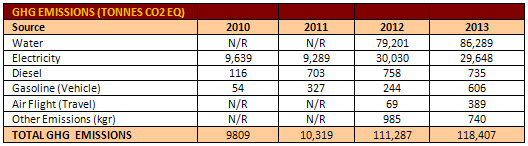

The following are the Green House

Gas Emissions (GHG) for ADCB from

2010 - 2013.

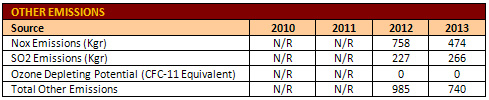

Table 4: ADCB GHG Related Emissions

Source: (ADCB, 2013, p.50).

Many ADCB operations involve staff

travelling with flights and the majority

are about a three-hour journey. In

2010, ADCB started monitoring the

mileage and possible emissions with

ozone depleting potential. The following

table shows the trends.

Table 5: ADCB Related Emissions

Source: (ADCB, 2013, p. 50).

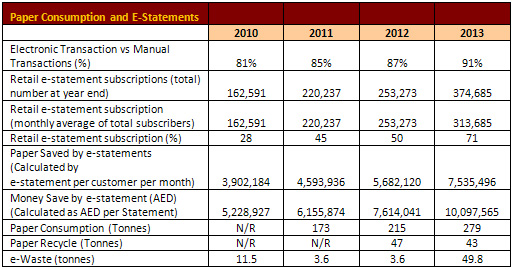

From 2013, as the ADCB electronic

transactions increase, the same happens

to the number of electronic statements

and the paper it saves by the same.

The Banks have realized huge savings

from the e-statements while the e-waste

has increased as shown in the table

below.

Table 6: E-Statement Savings

Source: (ADCB, 2013, p.51).

ADCB supports financial literacy by

engaging other stakeholders such as

the Emirates Foundation. This CSR

activity completed within the Q4-2013.

ADCB collaborates with various organizations,

which have environmental conservation

programs. These organizations include

EWWS-WWF and the Emirates foundation.

This initiative completed culminating

into the bigger Abu Dhabi Sustainability

Group (ADSG). ADCB uses sustainability

as a measure of prequalifying their

suppliers by providing them with a

questionnaire for assessment of their

procedures and status. ADCB managed

to lower the energy usage by 1.3%

in 2013. ADCB is in the process of

cutting back paper usage with the

30% rise in 2013 attributed to 48%

as customers were shifting to online

platforms to long term benefits. Finally,

ADCB deferred the waste recycling

programs to 2014 and the progress

will be captured in the 2015 reports

(ADCB, 2013).

CSR Activities

of Islamic Banks in UAE

Abu Dhabi Islamic Bank CSR Initiatives:

The ADIB CSR initiatives are managed

by a Council to integrate the banks'

business goals to the community and

employees. However, it is important

to state early that the ADIB investments

for CSR are not published according

to the findings in the last five years.

Most of the CSR activities are merely

described and qualified in successive

financial and sustainability annual

reports. Nevertheless, the ADIB recognized

the important of engaging in CSR as

a way of giving back to the community

(ADIB, 2014). ADIB participates in

public financial education since 2011,

by sponsoring programmes in high schools,

colleges and Universities. This initiative

is to empower people to make better

financial decisions in life with the

ability of confirming their progress

via an online portal. ADIB has a Business

Pulse where SMEs are provided with

financial information and assistance

to meet their needs. This portal also

brings together various business heads

who share their financial experiences

and challenges in their SME organizations

(ADIB, 2014). ADIB has invested heavily

in their workforce in recognition

of their human resource assets. This

initiative motivates the workforce

to give their best when handling banking

customers. ADIB encourages workforce

learning and career development by

motivating training opportunities

and financing appropriate courses.

ADIB encourages workforce diversity

because it enables close ties and

excellence in customer service. ADIB

nurtures the UAE local talents and

has been recognized for the efforts

with awards by the Emirates Institute

of Banking and Financial Studies (EIBFS).

ADIB has entered into collaboration

with various Higher Education Institutions

(HEIs) to further the Emiratization

policy that is active in the UAE.

By 2014, about 48% of ADIB workforces

were UAE locals in line with the Emiratization

goals (ADIB, 2014). ADIB is very active

in environmental conservation initiatives

to lower the 2014 carbon footprint

by 20% annually. Due to ADIB efforts

towards environmental responsibility,

the bank has LEED Pre-Certification

for Gold standards and is on its way

to other esteemed recognitions. ADIB

is active in minimizing paper materials

using E-Systems, recycles waste and

has invested in various energy saving

processes within the banking facilities

(ADIB, 2014).

In line with the Islamic banking work,

ADIB supports the annual Islamic Finance

Forum. ADIB also offers socio-economic

solutions to the Islamic Finance world

and offers rewards of up to $100,000

to winning innovators in an annual

competition with the 2014 event having

more than 200 entries. ADIB sponsors

Art and Science in Islam conferences

to make the public aware of opportunities

and history of their heritage. Around

Ramadhan period ADIB always provides

Iftar boxes to enable people to contribute

to the aid of the less fortunate in

the society. Collections are done

from major public transit areas like

Mosques, Banks and commuter areas.

ADIB is also very active in assisting

and sponsoring sports events. The

last event in 2014 had over 2000 children

participate in a football challenge.

Finally, ADIB (2014) sponsored mass

weddings to support people who are

unable to do so on their own and avoid

food wastage typical of such occasions.

Emirates Islamic Bank CSR Initiatives:

The Emirates Islamic Bank is active

if supporting social activities especially

around the Ramadhan period. The objective

is to create a lasting effect on the

society. The bank supports the Zakat

Fund Ramadhan Campaign (ZFRC) which

mandates all Muslims to donate to

the less fortunate people in society.

The bank supports the Al Ajer Initiative

(AAI) to enhance societal harmony

and promote forgiveness. The bank

has numerous multispectral collaborations

such as with the government, civil

society and non-government organizations

with the climax of activities happening

around Ramadhan period. The bank supports

Emirates Foundation for Youth Development

(EFYF) which undertakes numerous social

philanthropic activities to improve

public welfare. Finally, Emirates

Islamic bank collaborates with the

Dar Al Ber Society which is a leading

charity support organization to distribute

financial vouchers from AED 100-500

especially around the Ramadhan period

(Emirates Islamic Bank, 2013).

Methodology

The researcher applied mix qualitative

and quantitative methods in this study

(Saunders, et al., 2007). The qualitative

study was applied in the critical

literature review of the concept of

CSR in commercial and Islamic banks

in the UAE. This method was rational

considering that Islamic banks hardly

publish expenditures in CSR even though

there is literature to confirm they

undertake such activities. The Quantitative

method was used in the analysis of

impact of CSR to the commercial and

Islamic banks' profitability. This

method was justified because it is

easier to summarize data and draw

conclusions from trends. This study

on the impact of CSR to UAE banks'

profitability covered data from 2010

- 2014. This was rational because

the activities are current and the

impact is recognizable if not documented.

From the literature review, it is

clear that the concept of CSR differs

between the commercial banks and Islamic

banks in the UAE, hence the visible

differences in the profitability.

However, other issues like size of

bank could also be affected by the

impact analysis. In order to harmonize

the CSR effects and be able to generalize

for the sampled UAE banks on assumption

that some share customers, this study

adopted the KLD Research & Analytics

(KLD) (Bolton, 2013). Therefore, by

decomposing the available CSR data,

the research sought to establish its

effect on the sampled banks namely,

ADCB, ADIB and Emirates Islamic Banks.

The focus on CSR was on issues like

community initiatives, environmental

conservation, health and safety and

employee development. This research

was an analysis of the impact of CSR

on profitability hence the following

equation was applicable:

Profitability Performance = Direct

+ Indirect CRS Investments + Business

Therefore, KLD Profitability +

KLD CRS + KLD Business.

Analysis

ADCB Analysis of CSR on Profitability:

The ADCB CSR model resembles the intersecting

circles according to Geva (2008).

This is the analysis all the ADCB

functions such as economic policies,

ethical obligations, legal compliance

and philanthropic commitments are

all weighed by their customers to

determine their retention and eventually

the profitability (ADCB, 2014) as

shown in the figure and table below.

Figure 1: ADCB's Intersection Circles

CSR Model

Source: (Geva, 2008, Cited in Al-Tamimi,

2014, p.92).

The overall CSR changes at ADCB yielded

various outcomes related to profitability.

A summary of the effects of CSR at

ADCB is illustrated in Appendix I

(IFC, 2010) and the impact is minor.

The CSR at ADCB has created additional

knowledge to the management and board

on how to tighten governance and increase

profitability consistently. Such practices

attract new clients to ADCB via word

of mouth or publicity of the banks

from periodic financial statements

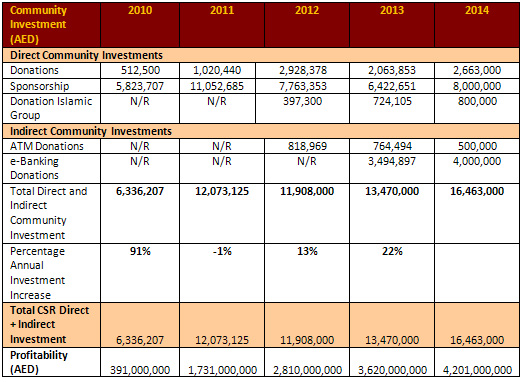

(IFC, 2010). Due to the numerous ADCB

CSR initiatives, the profit has been

rising yearly from AED 391 million

in 2010 to AED 4,201 billion in 2014.

For example, ADCB's direct investment

in CSR in 2013 was AED 7.79 million

as the bank shifted to e-statements

managed to save the bank over 7,535,500

pieces of paper and recycled 49.8

tonnes of e-waste. Additionally, the

ROE also increased from 1.54% in 2010

to 18.41% by 2014 (ADCB, 2014). The

following table shows the calculations

for ADCB using

Profitability Performance = Direct

+ Indirect CRS Investments + Business

Therefore, KLD Profitability =

KLD CRS + KLD Business

Table 7: KLD Profitability of ADCB

Islamic Bank

Analysis of CSR Impact on Profitability

Before delving into the Islamic banks

CRS impact proper, it is critical

to understand this concept in the

Islamic context. Generally Islamic

banking believes in collaboration

or Shirikah, which implies that CSR

is not separated or recognized as

a legal entity. Therefore, it appears

Islamic banks do not have a special

treatment or CSR activities which

perhaps indicates why most if not

all financial and sustainability reports

do not explicitly indicate the expenditures.

Islamic banking believes that CSR

is something which is natural and

an obligation, whether it is real

or abstract. Thus, stating the financial

expenditures on CSR would look like

imposing something that is assumed

to be already happening religiously

(Josuh, et al., 2015). Therefore,

under the Zimmah theory, CSR takes

place in Islamic banks on partnership

basis as opposed to business basis

as is typical with commercial banks.

Moreover, Islamic banks have a principle

of sharing loss and profits, therefore

their financial statements have huge

debt write offs equivalent to losses

(Al-Khuli, 2003).

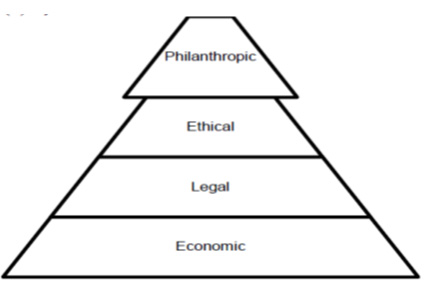

The ADIB model of CSR resembles the

pyramid model proposed by Geva (2008).

This is because there is more emphasis

on the economic stability of the bank,

followed by the legal, ethical then

philanthropic aspects (ADIB, 2014)

as shown in the figure and table below.

Table 8: ADIB CSR Investment vs.

Profitability

Figure 2: ADIB Pyramid Model of

CRS

Source: (Geva, 2008, Cited in Al-Tamimi,

2014, p.92).

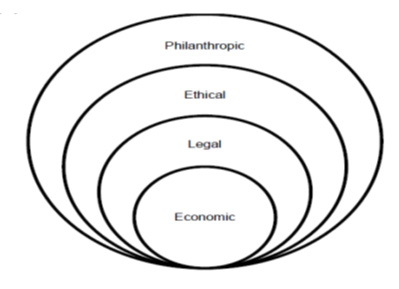

The Emirates Islamic Bank CRS model

resembles the concentric circles as

proposed by Geva (2008). This is because

even though the bank has economic

prosperity at the heart of the organization,

there is strong consideration for

legal compliance, ethical practices

and philanthropic activities (Emirates

Islamic Bank, 2004) as shown in the

table and figure below.

Figure 3: Emirates Islamic Bank

Concentric Circle CRS Model

Source: (Geva, 2008, Cited in

Al-Tamimi, 2014, p.92).

Table 9: Emirates Islamic Bank

CSR vs. Profitability

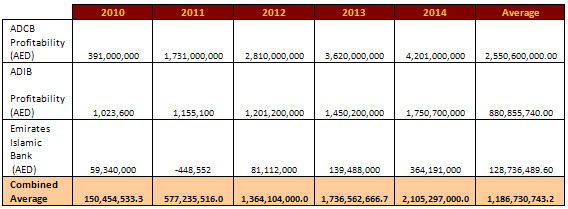

Then after the decomposition of the

annual CSR expenditure data with their

corresponding profitability, it was

established that the KLD impact was

greater among the commercial banks

than the Islamic Bank as indicated

in the table below.

Table 10: KLD Combined Profitability

Impact

Conclusion

In conclusion, various studies in

the last two decades support the view

that CSR activities in banks lead

to higher profitability. Nevertheless,

this only applies to specific CSR

activities especially when they align

to the banks' core activities and

business environment in the UAE. The

studies show that CSR creates a strong

bond between the banks and their stakeholders

who pool their capital leading to

banks stronger investment options

and profitability (Bolton, 2013).

The study established the CSR impact

is greater in commercial banks as

compared to the Islamic bank. This

was attributed to the Islamic banks

ideas of understanding and implementing

CSR as well as concept of profitability

where the banks undertake to share

losses and profits.

The ADCB CRS approach anchors on sustainable

business coexistence with the community

and environment. Therefore, ADCB has

established strong partnerships at

these levels by investing into worthy

causes that will leave a lasting socio-economic

effect within the national market

while conserving the environment.

This paper concludes that the ADCB,

which follows the intersecting circles

CSR model, could be contributing to

minor annual increments in profitability

even though regression analysis has

been accomplished to date on the same

(IFC, 2010, ADCB, 2010; 2014) as shown

in Appendix I. However, the paper

concluded that the CSR accomplished

in Islamic counterparts namely ADIB

and Emirates Bank have no significant

impact on the profitability (El Mosaid

and Boutti, 2012). The ADIB pyramid

CRS model has actually yielded higher

annual profitability while the Emirates

Islamic Bank's concentric circle CSR

model yields moderate profits as compared

to the other two banks.

The current study merely had descriptive

commitment and barely any data to

compare with the profitability of

the Islamic banks and this trend seemed

to be widespread when the researcher

was searching for similar information.

References

Abu Dhabi Islamic Bank (2014). Annual

Report. Retrieved October 9, 2015,

from

http://www.adib.ae/sites/default/files/Annual_Report_2014.pdf

ADCB (2014). Annual Report. Retrieved

October 7, 2015, from

http://www.adcb.com/about/investorrelations/financialinformation/ARsite/2014/downloads/

ADCB_AR14_English.pdf

ADCB (2013). Ambition and Sustainability

Report. Retrieved October 7, 2015,

from

http://static.globalreporting.org/report-pdfs/2014/4e996bf251182082048123c0c00c6438.pdf

ADCB (2010). Annual Report. Retrieved

October 7, 2015, from

http://www.adcb.com/arabic/images/Annual%20report%202010%20english_tcm10-28681.pdf

Ahmed, S.U., Islam, M.Z. & Hasan,

I., (2012). Corporate social responsibility

and

financial performance linkage - evidence

from the banking sector of Bangladesh.

Journal of Organization Management,

1(1); 14-21.

Anderson, A., Myers, D., (2007). The

cost of being good. Review of Business,

28(1),

5-17.

Al-Khuli, A. M. (2003). Nazariyyah

al-Shakhsiyyah al-I'tibariyyah baina

al-Fiqhi al-

Islami wa al-Qanun al-Wadh'i. Al-Qahirah:

Dar al-Salam

Al-Tamimi, H. A. H. (2014). Corporate

Social Responsibility Practices of

UAE Banks.

Global Journal of Business Research,

8(3); 91-108.

Blowfield, M. & Murray, A. (2008).

Corporate Responsibility: A Critical

Introduction.

Oxford: Oxford University Press.

Bolton, B. J., (2013 June). Corporate

Social Responsibility and Bank Performance.

Retrieved October 7, 2015, from http://dx.doi.org/10.2139/ssrn.2277912

Cai, Y., Jo, H. & Pan, C., (2012).

Doing well while doing bad? CSR in

controversial

industry sectors. Journal of Business

Ethics, 108(2); 467-480.

Carroll, A.B., (1979). A three-dimensional

conceptual model of corporate social

responsibility. Academy of Management

Review, 4(4); 497-505.

Cheng, B., Ioannou, I. & Serafeim,

G., (2011). Corporate Social Responsibility

and

Access to Finance. Strategic Management

Journal.

Deckop, J., Merriman, K. & Gupta,

S. (2006). The effects of CEO pay

structure on

corporate social performance. Journal

of Management, 32(3); 329-342.

El Ghoul, S., Guedhami, O., Kwok,

C., & Mishra, D. (2011). Does

corporate social

responsibility affect the cost of

capital? Journal of Banking &

Finance, 35(9), 2388-2406.

El Mosaid, F. & Boutti, R. (2012).

Relationship Between Corporate Social

Responsibility

and Financial Performance in Islamic

Banking. Research Journal of Finance

and Accounting.

3(10); 93-103.

Emirates Islamic Bank (2014). Annual

Report. Retrieved October 9, 2015,

from

http://www.emiratesislamicbank.ae/assets/cms/docs/EIB/EI-AnnualReport2014_%20Eng_V1.pdf

Emirates Islamic Bank (2013). Emirates

Islamic bank Supports Key Social Activities

During the Holy Month of Ramadhan.

Emirates Islamic Group. Retrieved

15 October 2015, from http://www.emiratesislamicbank.ae/en/latestnews/2013/august/news04082013.cfm

Freeman, R.A., (1984). Strategic Management:

A Stakeholder Approach. Boston: Pitman.

Gande, A. & Kalpathy, S., (2012).

CEO compensation at financial firms.

Southern

Methodist University.

Geva, A. (2008), Three Models of Corporate

Social Responsibility: Interrelationships

between Theory, Research, and Practice,

Center for Business Ethics at Bentley

College,

Blackwell Publishing.

Griffin, J. & Mahon, J., (1997).

The corporate social performance and

corporate financial

performance debate. Twenty-five years

of incomparable research. Business

and Society, 36(1), 5-31.

Hawa, N. (2012). Factors Shaping the

Definition and Practice of Corporate

Social Responsibility at

Local Banks in the United Arab Emirates.

MSc Post Graduate Dissertation in

Corporate Governance

& Business Ethics. Retrieved October

7, 2015, from

http://www.lccge.bbk.ac.uk/publications-and-resources/docs/Nadine-Hawa-MSc-Dissertation.pdf

IFC (2010). Corporate Governance Success

Stories. IFC Advisory Services in

the Middle

East and North Africa. Retrieved October

7, 2015, from http://www.ifc.org/wps/wcm/connect/0e4f7b80401cf57abb43ff23ff966f85/Corporate_Governance_

Success_Stories_MENA.pdf?MOD=AJPERES

International Monetary Fund (IMF).

(2007). International Monetary Fund's

(IMF) 2007 Financial

System Stability Assessment. Retrieved

October 7, 2015, from

http://www.imf.org/external/pubs/ft/scr/2007/cr07357.pdf.

Jusoh, W. N. H. W., Ibrahim, U. &

Napiah, M. D.M (2015). An Islamic

Perspective on

Corporate Social Responsibility of

Islamic Banks. Mediterranean Journal

of Social Sciences,

6(2); 308 - 315.

Orlitzky, M. Schmidt, F.L., Rynes,

S.L. (2003). Corporate and financial

performance: a meta-analysis. Organization

Studies, 24(3), 403-441.

Saunders, M., Lewis, P. & Thornhill,

A. (2007). Research Methods for Business

Students. 4th ed.

London: Prentice Hall.

Scholtens, B. (2009). Corporate social

responsibility in the international

banking industry.

Journal of Business Ethics, 86(2),

159-175.

Shen, C.H. & Chang, Y. (2009).

Ambition versus conscience, does corporate

social responsibility

pay off? The application of matching

methods. Journal of Business Ethics,

88(1); 133-153.

Sigurthorsson, D. (2012). The Icelandic

banking crisis: a reason to rethink

CSR?

Journal of Business Ethics, 111(2);

147-156.

|